Receivership vs Bankruptcy: Which Is Right for Your Business?

A quick guide to choosing bankruptcy or receivership and why timing matters.

Date:

November 24, 2025

Category:

Bankruptcy & Receivership

Follow us on social media:

Follow us on social media:

Business bankruptcy filings surged to 23,107 cases in 2024, a 22.1% year-over-year increase and the highest business-filing total since 2017.

At the same time, U.S. corporate bankruptcies reached 694 cases, the highest annual corporate count since 2010, driven by elevated interest rates and a wave of debt maturities hitting overleveraged borrowers.

Yet bankruptcy isn't the only option for distressed businesses.

State court receiverships are "now poised to take center stage" as the preferred method for addressing financial distress in small and mid-sized companies, according to the American Bankruptcy Institute Journal.

With Illinois enacting a comprehensive Receivership Act effective January 2026, the number of states with modern commercial receivership frameworks rises to at least 14.

The choice between bankruptcy and receivership carries heightened strategic importance.

This comparison examines both remedies through the lens of data, including timelines, costs, recovery rates, and success probabilities, which inform strategic decision-making for lenders, investors, and business stakeholders navigating distressed situations.

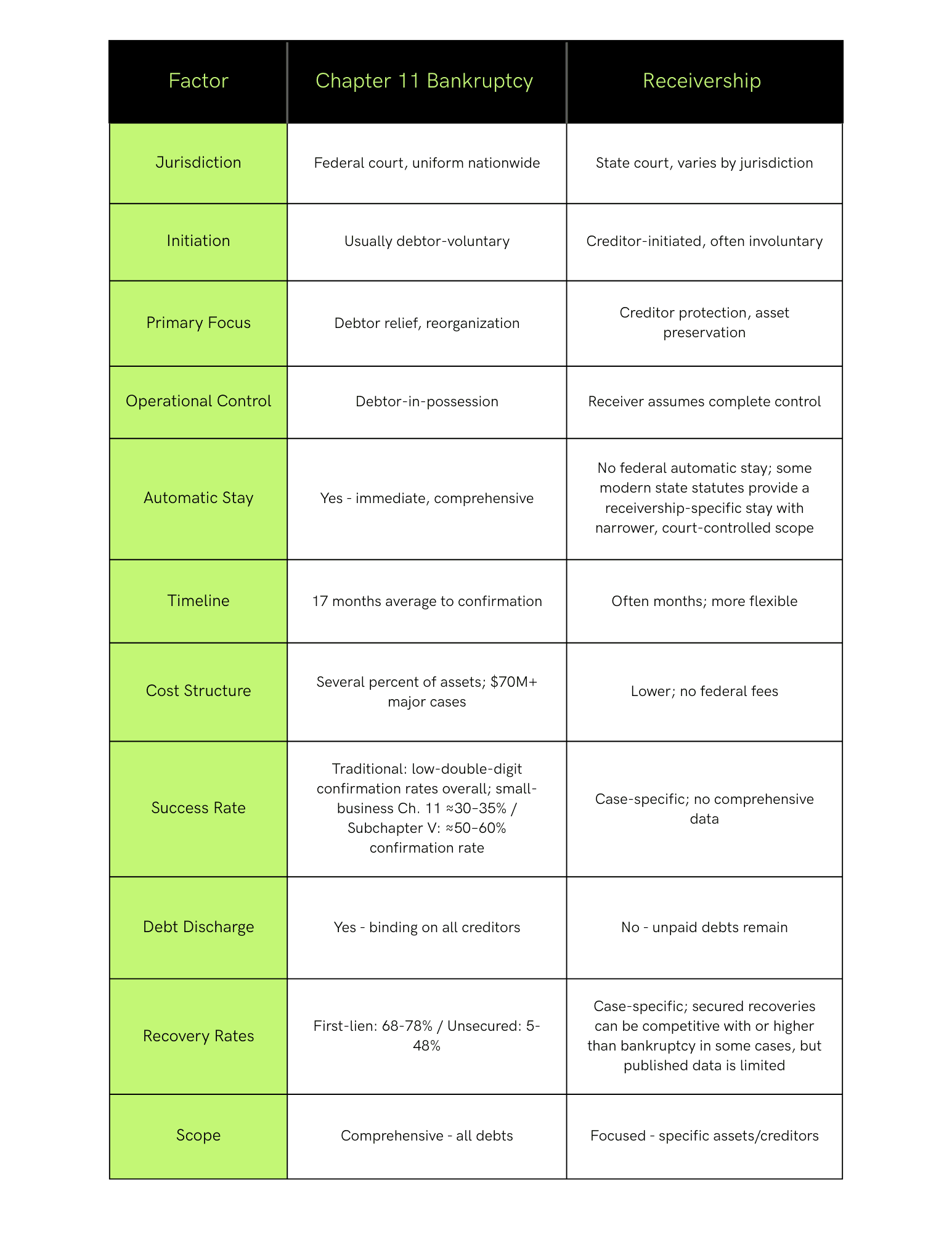

Chapter 11 Bankruptcy: The Federal Framework

Chapter 11 bankruptcy provides a federal legal process for business reorganization under court supervision. The debtor typically remains in control as a "debtor-in-possession" while formulating a restructuring plan, in contrast to Chapter 7 liquidation, where a trustee sells assets and distributes proceeds to creditors.

The automatic stay takes effect immediately upon filing, halting virtually all creditor collection actions, foreclosures, and lawsuits. This breathing room allows the debtor to negotiate with creditors and propose a reorganization plan.

For eligible businesses with debts under $3,024,725 (approximately $3.0 million, indexed for inflation), Subchapter V offers a streamlined process with compressed timelines and eliminates creditors' committees.

The Reality: Success Rates and Timelines

Empirical studies and practitioner surveys generally find that only a small minority (roughly low-double-digit percentages) of Chapter 11 cases result in a confirmed reorganization plan, with the remainder being liquidated or dismissed.

Historical data from 2010 to 2019 show that 70% of small businesses bypass reorganization attempts entirely and file Chapter 7 directly.

Of small businesses that do attempt traditional Chapter 11, only approximately 33% successfully reorganize. The rest fail to confirm a viable plan.

Subchapter V dramatically improves these odds, with roughly 56% of cases confirming a plan, compared with about 30-35% for traditional small-business Chapter 11 cases. This improvement reflects the elimination of the absolute priority rule, exemption from quarterly U.S. Trustee fees, and the fact that official creditors' committees are uncommon and appointed only in limited circumstances.

However, the June 21, 2024, sunset of the temporary $7.5 million cap, which caused the debt limit to revert to its inflation-adjusted baseline of $3,024,725, significantly curtailed eligibility for thousands of mid-sized businesses.

Timeline expectations require careful planning. Chapter 11 cases average 17 months from filing to plan confirmation, though complex cases routinely extend to five years or longer.

After confirmation, payment plans typically run an additional 3-5 years, meaning creditors often wait 2-6 years for full recovery from the date of the petition.

Prepackaged bankruptcies, where debtors negotiate plans with major creditors prior to filing, can emerge far faster - recent cases, such as Joann Inc., confirmed plans in 41 days. However, traditional contested Chapter 11 cases typically face an average timeline of 17 months.

Cost Structure and Administrative Expenses

Studies of significant Chapter 11 cases typically find that professional fees and other direct costs consume several percent of the estate's asset value, often in the low to mid-single digits, with complex cases sometimes running higher.

Major bankruptcies see eight-figure professional fees - Sullivan & Cromwell earned over $130 million after 10 months on FTX's bankruptcy, while Weil Gotshal collected nearly $70 million on a single 2024 engagement.

Beyond professional fees, debtors pay quarterly U.S. Trustee fees based on disbursements, as well as fees for creditors' committee professionals (despite having no control over their retention or billing), and ongoing business operating costs that receive administrative expense priority. These administrative expenses are paid before secured creditor distributions in many scenarios, directly eroding recovery.

Recovery Rates by Creditor Class

Secured first-lien creditors recovered an average of 68-78% in recent years, according to comprehensive tracking by BankruptcyData and S&P Global, though individual cases show significant variance based on collateral coverage and intercreditor dynamics.

Second-lien secured debt recovery averaged 50% in the first half of 2023, but the range is dramatic - some cases see a 5% recovery, while others approach 70%. The gap between first-lien and second-lien recoveries can span 18 to 68 percentage points, depending on asset coverage and whether intercreditor agreements include hard caps on first-lien principal increases through DIP financing.

Senior unsecured creditors face materially lower recoveries. The first nine months of 2023 saw senior unsecured recovery rates plummet to approximately 5% on average, driven by retail collapses like Bed Bath & Beyond (≤2.5% recovery) and Party City (<2% recovery). Longer-term averages indicate a 29-48% recovery, but recent distressed retail cases tend to skew toward the lower end.

Notably, distressed exchanges produce meaningfully higher recoveries than bankruptcy for senior unsecured creditors, with an average recovery of 54% via out-of-court exchange versus 43% via bankruptcy proceedings. This 11 percentage point difference explains the surge in liability management exercises that outnumbered bankruptcies 2-to-1 in 2024.

DIP Financing Market Bifurcation

Debtor-in-possession financing remained widely available throughout 2024-2025 but at sharply bifurcated pricing.

High-functioning businesses with temporary liquidity issues obtained DIP facilities at 3-5% interest with minimal fees. Truly distressed situations faced rates exceeding 15%.

Ligado Networks' $939 million DIP carried 17.5% PIK interest plus 15.5% cash interest.

Jackson Hospital, Wilson Creek Energy, and White Forest Resources all obtained DIPs with interest rates above 15%.

Quality borrowers, such as Mondee Holdings, secured facilities with only 0.52% fees and single-digit interest rates.

The 1,000+ basis point spread between distressed and quality DIP pricing reflects lender perception of ongoing cash burn and uncertain viability.

Receivership: The State Court Alternative

Receivership provides a state court remedy where a judge appoints an independent receiver to take custody of and manage a business's assets. Unlike bankruptcy, receivership is typically initiated by creditors and focuses on asset preservation rather than debtor relief.

The receiver acts as a neutral fiduciary with complete operational control. Existing management is sidelined - the receiver makes decisions on running the business, handling finances, and if authorized, selling assets or the company as a going concern.

There is no federal automatic stay and no debt discharge, although some modern state receivership statutes (including UCRERA and Illinois) provide a receivership-specific stay with more limited scope than the Bankruptcy Code's automatic stay. The goal is to maximize asset value for creditor's benefit.

Deployment Scenarios

Secured lender enforcement represents the most common receivership scenario. When a borrower defaults and a secured creditor fears collateral deterioration or diversion, the lender petitions the court to appoint a receiver. The receiver secures the collateral, continues operations if viable, and prepares for either an asset sale or a turnaround.

Fraud or mismanagement cases warrant immediate receiver appointment to prevent further waste. Courts frequently appoint receivers in cases involving embezzlement, Ponzi schemes, or gross mismanagement. The receiver preserves assets and records while investigations proceed.

Shareholder or partnership disputes can paralyze a business. When ownership conflicts prevent coherent management, a court-appointed receiver provides neutral stewardship, preventing business collapse during litigation.

Industries where federal bankruptcy is not an option must utilize state remedies. Because marijuana remains a Schedule I controlled substance under federal law, U.S. bankruptcy courts routinely dismiss cases involving plant-touching cannabis businesses, effectively making federal bankruptcy relief unavailable to much of the industry.

With a multi-billion-dollar cannabis debt maturity wall approaching 2026, distressed operators generally must rely on state-law tools - such as receiverships, assignments for the benefit of creditors, and out-of-court workouts - rather than Chapter 11.

Recent Legal Developments

The receivership legal landscape underwent a significant transformation in 2024-2025. Illinois enacted a comprehensive Receivership Act, signed by Governor Pritzker in August 2025, which took effect on January 1, 2026.

The Act replaces Illinois' previous four-sentence statute with a modern framework that grants receivers broad powers, including ongoing business management, the power of sale, audit authority, and subpoena power.

Illinois joins a growing group of at least 13 other states that have adopted UCRERA or similar commercial receivership statutes, including Alabama, Arizona, Connecticut, Florida, Maryland, Michigan, Nevada, North Carolina, Oregon, Rhode Island, Tennessee, Utah, and West Virginia.

These uniform acts provide statutory roadmaps for appointment, receiver powers, asset sales, notice requirements, and creditor priorities, eliminating the need to parse inconsistent case law.

A critical April 2024 decision from the U.S. Bankruptcy Court for the Middle District of Tennessee in In re 530 Donelson, LLC established that state court receivership orders granting receivers broad authority do not automatically deprive LLC managing members of their constitutional right to file bankruptcy. General language granting broad powers proved insufficient to strip bankruptcy filing rights. 530 Donelson confirms that general, broad-powers receivership language is not enough to strip bankruptcy filing authority from LLC managing members. Lenders hoping to limit a debtor's ability to file must pay close attention to corporate authority and governance provisions. However, even explicit prepetition restrictions on the right to file are often scrutinized or refused enforcement on public policy grounds.

Operational Advantages

Speed often proves decisive.

A receivership can be established within days or weeks through a court motion, and once appointed, a receiver can act immediately to safeguard assets. Resolution often occurs in months, rather than the 17+ month average in Chapter 11.

A lower cost structure makes receivership more attractive for mid-market companies. There are no federal filing fees, no quarterly U.S. Trustee fees, and no mandatory creditors' committees. The process involves fewer court hearings and less procedural complexity.

Receiver compensation is often structured as hourly rates (frequently in the $250–$400+ range) or percentage-based compensation on recoveries, subject to court approval and local market practice. This compensation is substantial but generally lower than bankruptcy administrative expenses as a percentage of the estate value.

Creditor control differentiates receivership from debtor-driven bankruptcy. The moving creditor often nominates a receiver they trust, frequently an industry expert who can implement turnaround strategies or prepare the business for sale. This professional management instills confidence in stakeholders that the situation is being handled responsibly.

Strategic Comparison: Decision Framework

Understanding the structural differences between bankruptcy and receivership informs the selection of remedies.

Speed versus protection trade-offs require careful evaluation. Bankruptcy's immediate automatic stay provides a comprehensive freeze on creditors, but the lengthy process erodes value through professional fees, business disruption, and customer/employee attrition.

Receivership offers a faster resolution but lacks the comprehensive protection of the automatic stay.

Cost reality impacts stakeholder recoveries. Bankruptcy administrative expenses, including the fees of creditors' committee professionals, quarterly U.S. Trustee fees, and extensive professional fees, are paid before secured creditor distributions. This administrative expense burden can consume a significant amount of value.

Receivership's streamlined structure preserves more value for stakeholders by eliminating federal fees and mandatory committees.

Industry-specific drivers increasingly determine remedy selection. Cannabis companies generally must rely on state-law remedies such as receiverships, assignments for the benefit of creditors, and out-of-court workouts, given that federal bankruptcy courts routinely dismiss cases involving plant-touching businesses.

UCRERA and UCRERA-style states offer standardized receivership procedures that rival bankruptcy's efficiency for real estate-related businesses. Fintech lenders post-Synapse may favor receivership's faster asset recovery over protracted bankruptcy timelines.

Making the Strategic Choice

Remedy selection depends on creditor structure, debt composition, timeline urgency, and desired outcomes.

Choose Chapter 11 Bankruptcy When:

Multiple creditor classes with competing interests require comprehensive resolution. Bankruptcy provides a single forum to address secured debt, unsecured bondholders, trade creditors, and litigation claims under court-supervised priority rules.

Automatic stay is essential for businesses facing multiple foreclosures, lawsuits, or aggressive collection actions. The immediate, comprehensive creditor freeze provides critical breathing room.

Debt discharge represents the primary goal. When overwhelming unsecured liabilities require elimination rather than just asset preservation, bankruptcy's discharge power is indispensable.

Contract rejection capabilities are needed. Bankruptcy enables debtors to reject unfavorable leases or agreements with court approval, thereby shedding obligations that impair their viability.

Actual reorganization is the objective. If the goal is to restructure debt and continue the business in the long term under existing ownership, Chapter 11 provides the legal framework for plan confirmation and implementation.

Subchapter V eligibility exists (debt under $3,024,725). The 56% plan confirmation rate, compared to traditional Chapter 11's lower success rates, makes Subchapter V materially more attractive for eligible businesses.

Choose Receivership When:

Single or a few secured creditors dominate the situation. When one lender holds most of the leverage and other creditors are limited, receivership provides focused asset preservation without the complexity of comprehensive bankruptcy.

Speed is paramount. For rapidly deteriorating assets, fraud risk, or market timing considerations, receivership's ability to deploy within days and resolve within months proves decisive.

Cost preservation is critical. Mid-market companies, where Chapter 11's several-percent fee burden would consume disproportionate value, benefit from the receivership's lower cost structure.

Creditor control is preferred. Secured lenders wanting an industry-expert receiver to manage operations and prepare for sale can nominate receivers and steer the process more directly than in debtor-driven bankruptcy.

Federal bankruptcy is unavailable or inadvisable. Cannabis operators, certain regulated entities, or businesses where bankruptcy filing triggers contract terminations must pursue state remedies.

Asset sale is the primary goal rather than comprehensive debt restructuring. Receivership facilitates the efficient sale of going-concern businesses or orderly liquidations.

Industry-Specific Considerations

Cannabis operators face unique constraints. Federal bankruptcy remains unavailable due to marijuana's Schedule I status, with bankruptcy courts routinely dismissing cases involving plant-touching cannabis businesses. The multi-billion-dollar debt maturity wall approaching 2026 creates acute pressure for refinancing. Receivership represents the primary viable restructuring path, though state-specific licensing requirements for receivers add operational complexity. Only operators maintaining early creditor dialogue, strict cash discipline, and proven store-level EBITDA are expected to navigate the shakeout.

Secured lenders focus on maximizing collateral recovery. First-lien positions recovering 68-78% drive strategy, with intercreditor agreement terms proving critical. Receivership avoids bankruptcy administrative expense dilution that erodes secured creditor recovery. Following In re 530 Donelson, lenders should recognize that receivership orders, even with broad powers, do not automatically prevent the debtor from later filing bankruptcy.

Small businesses face stark choices. Those with debt under $3,024,725 should carefully evaluate the 56% plan confirmation rate of Subchapter V before opting for traditional Chapter 11. Businesses exceeding the Subchapter V limit often find receivership more cost-effective than conventional Chapter 11, which sees plan confirmation in only low-double-digit percentages of cases while consuming several percent of assets in fees.

Sources

Bankruptcy Filing Statistics:

S&P Global Market Intelligence, "US corporate bankruptcies soar to 14-year high in 2024"

Epiq Global, "Total Bankruptcy Filings Increased 10 Percent in the First Half of 2025"

Default Rates and Recovery Data:

S&P Global, "2024 Annual Global Corporate Default And Rating Transition Study"

S&P Global Ratings, "North American Debt Recoveries May Trend Down For Longer"

Legal Analysis:

Proskauer Rose, "The Evolving New Normal: 2024 Private Credit Restructuring Year in Review"

Florida Bar Journal, "Florida's New Commercial Real Estate Receivership Act"

DIP Financing:

Subchapter V Analysis:

University of Connecticut Finance Research, "Small Business Reorganization Act Analysis"

U.S. Department of Justice, U.S. Trustee Program, "Subchapter V Small Business Debtor Cases"

Cannabis Industry:

Cannabis Law Now, "Cannabis Receiverships Are and Will Be on the Rise"

Crain's Detroit Business, "Top cannabis companies lost $2B in 2024"

MJBizDaily, "Fed rate cut could be game changer as cannabis industry debt maturity looms"

Government and Court Sources:

Business bankruptcy filings surged to 23,107 cases in 2024, a 22.1% year-over-year increase and the highest business-filing total since 2017.

At the same time, U.S. corporate bankruptcies reached 694 cases, the highest annual corporate count since 2010, driven by elevated interest rates and a wave of debt maturities hitting overleveraged borrowers.

Yet bankruptcy isn't the only option for distressed businesses.

State court receiverships are "now poised to take center stage" as the preferred method for addressing financial distress in small and mid-sized companies, according to the American Bankruptcy Institute Journal.

With Illinois enacting a comprehensive Receivership Act effective January 2026, the number of states with modern commercial receivership frameworks rises to at least 14.

The choice between bankruptcy and receivership carries heightened strategic importance.

This comparison examines both remedies through the lens of data, including timelines, costs, recovery rates, and success probabilities, which inform strategic decision-making for lenders, investors, and business stakeholders navigating distressed situations.

Chapter 11 Bankruptcy: The Federal Framework

Chapter 11 bankruptcy provides a federal legal process for business reorganization under court supervision. The debtor typically remains in control as a "debtor-in-possession" while formulating a restructuring plan, in contrast to Chapter 7 liquidation, where a trustee sells assets and distributes proceeds to creditors.

The automatic stay takes effect immediately upon filing, halting virtually all creditor collection actions, foreclosures, and lawsuits. This breathing room allows the debtor to negotiate with creditors and propose a reorganization plan.

For eligible businesses with debts under $3,024,725 (approximately $3.0 million, indexed for inflation), Subchapter V offers a streamlined process with compressed timelines and eliminates creditors' committees.

The Reality: Success Rates and Timelines

Empirical studies and practitioner surveys generally find that only a small minority (roughly low-double-digit percentages) of Chapter 11 cases result in a confirmed reorganization plan, with the remainder being liquidated or dismissed.

Historical data from 2010 to 2019 show that 70% of small businesses bypass reorganization attempts entirely and file Chapter 7 directly.

Of small businesses that do attempt traditional Chapter 11, only approximately 33% successfully reorganize. The rest fail to confirm a viable plan.

Subchapter V dramatically improves these odds, with roughly 56% of cases confirming a plan, compared with about 30-35% for traditional small-business Chapter 11 cases. This improvement reflects the elimination of the absolute priority rule, exemption from quarterly U.S. Trustee fees, and the fact that official creditors' committees are uncommon and appointed only in limited circumstances.

However, the June 21, 2024, sunset of the temporary $7.5 million cap, which caused the debt limit to revert to its inflation-adjusted baseline of $3,024,725, significantly curtailed eligibility for thousands of mid-sized businesses.

Timeline expectations require careful planning. Chapter 11 cases average 17 months from filing to plan confirmation, though complex cases routinely extend to five years or longer.

After confirmation, payment plans typically run an additional 3-5 years, meaning creditors often wait 2-6 years for full recovery from the date of the petition.

Prepackaged bankruptcies, where debtors negotiate plans with major creditors prior to filing, can emerge far faster - recent cases, such as Joann Inc., confirmed plans in 41 days. However, traditional contested Chapter 11 cases typically face an average timeline of 17 months.

Cost Structure and Administrative Expenses

Studies of significant Chapter 11 cases typically find that professional fees and other direct costs consume several percent of the estate's asset value, often in the low to mid-single digits, with complex cases sometimes running higher.

Major bankruptcies see eight-figure professional fees - Sullivan & Cromwell earned over $130 million after 10 months on FTX's bankruptcy, while Weil Gotshal collected nearly $70 million on a single 2024 engagement.

Beyond professional fees, debtors pay quarterly U.S. Trustee fees based on disbursements, as well as fees for creditors' committee professionals (despite having no control over their retention or billing), and ongoing business operating costs that receive administrative expense priority. These administrative expenses are paid before secured creditor distributions in many scenarios, directly eroding recovery.

Recovery Rates by Creditor Class

Secured first-lien creditors recovered an average of 68-78% in recent years, according to comprehensive tracking by BankruptcyData and S&P Global, though individual cases show significant variance based on collateral coverage and intercreditor dynamics.

Second-lien secured debt recovery averaged 50% in the first half of 2023, but the range is dramatic - some cases see a 5% recovery, while others approach 70%. The gap between first-lien and second-lien recoveries can span 18 to 68 percentage points, depending on asset coverage and whether intercreditor agreements include hard caps on first-lien principal increases through DIP financing.

Senior unsecured creditors face materially lower recoveries. The first nine months of 2023 saw senior unsecured recovery rates plummet to approximately 5% on average, driven by retail collapses like Bed Bath & Beyond (≤2.5% recovery) and Party City (<2% recovery). Longer-term averages indicate a 29-48% recovery, but recent distressed retail cases tend to skew toward the lower end.

Notably, distressed exchanges produce meaningfully higher recoveries than bankruptcy for senior unsecured creditors, with an average recovery of 54% via out-of-court exchange versus 43% via bankruptcy proceedings. This 11 percentage point difference explains the surge in liability management exercises that outnumbered bankruptcies 2-to-1 in 2024.

DIP Financing Market Bifurcation

Debtor-in-possession financing remained widely available throughout 2024-2025 but at sharply bifurcated pricing.

High-functioning businesses with temporary liquidity issues obtained DIP facilities at 3-5% interest with minimal fees. Truly distressed situations faced rates exceeding 15%.

Ligado Networks' $939 million DIP carried 17.5% PIK interest plus 15.5% cash interest.

Jackson Hospital, Wilson Creek Energy, and White Forest Resources all obtained DIPs with interest rates above 15%.

Quality borrowers, such as Mondee Holdings, secured facilities with only 0.52% fees and single-digit interest rates.

The 1,000+ basis point spread between distressed and quality DIP pricing reflects lender perception of ongoing cash burn and uncertain viability.

Receivership: The State Court Alternative

Receivership provides a state court remedy where a judge appoints an independent receiver to take custody of and manage a business's assets. Unlike bankruptcy, receivership is typically initiated by creditors and focuses on asset preservation rather than debtor relief.

The receiver acts as a neutral fiduciary with complete operational control. Existing management is sidelined - the receiver makes decisions on running the business, handling finances, and if authorized, selling assets or the company as a going concern.

There is no federal automatic stay and no debt discharge, although some modern state receivership statutes (including UCRERA and Illinois) provide a receivership-specific stay with more limited scope than the Bankruptcy Code's automatic stay. The goal is to maximize asset value for creditor's benefit.

Deployment Scenarios

Secured lender enforcement represents the most common receivership scenario. When a borrower defaults and a secured creditor fears collateral deterioration or diversion, the lender petitions the court to appoint a receiver. The receiver secures the collateral, continues operations if viable, and prepares for either an asset sale or a turnaround.

Fraud or mismanagement cases warrant immediate receiver appointment to prevent further waste. Courts frequently appoint receivers in cases involving embezzlement, Ponzi schemes, or gross mismanagement. The receiver preserves assets and records while investigations proceed.

Shareholder or partnership disputes can paralyze a business. When ownership conflicts prevent coherent management, a court-appointed receiver provides neutral stewardship, preventing business collapse during litigation.

Industries where federal bankruptcy is not an option must utilize state remedies. Because marijuana remains a Schedule I controlled substance under federal law, U.S. bankruptcy courts routinely dismiss cases involving plant-touching cannabis businesses, effectively making federal bankruptcy relief unavailable to much of the industry.

With a multi-billion-dollar cannabis debt maturity wall approaching 2026, distressed operators generally must rely on state-law tools - such as receiverships, assignments for the benefit of creditors, and out-of-court workouts - rather than Chapter 11.

Recent Legal Developments

The receivership legal landscape underwent a significant transformation in 2024-2025. Illinois enacted a comprehensive Receivership Act, signed by Governor Pritzker in August 2025, which took effect on January 1, 2026.

The Act replaces Illinois' previous four-sentence statute with a modern framework that grants receivers broad powers, including ongoing business management, the power of sale, audit authority, and subpoena power.

Illinois joins a growing group of at least 13 other states that have adopted UCRERA or similar commercial receivership statutes, including Alabama, Arizona, Connecticut, Florida, Maryland, Michigan, Nevada, North Carolina, Oregon, Rhode Island, Tennessee, Utah, and West Virginia.

These uniform acts provide statutory roadmaps for appointment, receiver powers, asset sales, notice requirements, and creditor priorities, eliminating the need to parse inconsistent case law.

A critical April 2024 decision from the U.S. Bankruptcy Court for the Middle District of Tennessee in In re 530 Donelson, LLC established that state court receivership orders granting receivers broad authority do not automatically deprive LLC managing members of their constitutional right to file bankruptcy. General language granting broad powers proved insufficient to strip bankruptcy filing rights. 530 Donelson confirms that general, broad-powers receivership language is not enough to strip bankruptcy filing authority from LLC managing members. Lenders hoping to limit a debtor's ability to file must pay close attention to corporate authority and governance provisions. However, even explicit prepetition restrictions on the right to file are often scrutinized or refused enforcement on public policy grounds.

Operational Advantages

Speed often proves decisive.

A receivership can be established within days or weeks through a court motion, and once appointed, a receiver can act immediately to safeguard assets. Resolution often occurs in months, rather than the 17+ month average in Chapter 11.

A lower cost structure makes receivership more attractive for mid-market companies. There are no federal filing fees, no quarterly U.S. Trustee fees, and no mandatory creditors' committees. The process involves fewer court hearings and less procedural complexity.

Receiver compensation is often structured as hourly rates (frequently in the $250–$400+ range) or percentage-based compensation on recoveries, subject to court approval and local market practice. This compensation is substantial but generally lower than bankruptcy administrative expenses as a percentage of the estate value.

Creditor control differentiates receivership from debtor-driven bankruptcy. The moving creditor often nominates a receiver they trust, frequently an industry expert who can implement turnaround strategies or prepare the business for sale. This professional management instills confidence in stakeholders that the situation is being handled responsibly.

Strategic Comparison: Decision Framework

Understanding the structural differences between bankruptcy and receivership informs the selection of remedies.

Speed versus protection trade-offs require careful evaluation. Bankruptcy's immediate automatic stay provides a comprehensive freeze on creditors, but the lengthy process erodes value through professional fees, business disruption, and customer/employee attrition.

Receivership offers a faster resolution but lacks the comprehensive protection of the automatic stay.

Cost reality impacts stakeholder recoveries. Bankruptcy administrative expenses, including the fees of creditors' committee professionals, quarterly U.S. Trustee fees, and extensive professional fees, are paid before secured creditor distributions. This administrative expense burden can consume a significant amount of value.

Receivership's streamlined structure preserves more value for stakeholders by eliminating federal fees and mandatory committees.

Industry-specific drivers increasingly determine remedy selection. Cannabis companies generally must rely on state-law remedies such as receiverships, assignments for the benefit of creditors, and out-of-court workouts, given that federal bankruptcy courts routinely dismiss cases involving plant-touching businesses.

UCRERA and UCRERA-style states offer standardized receivership procedures that rival bankruptcy's efficiency for real estate-related businesses. Fintech lenders post-Synapse may favor receivership's faster asset recovery over protracted bankruptcy timelines.

Making the Strategic Choice

Remedy selection depends on creditor structure, debt composition, timeline urgency, and desired outcomes.

Choose Chapter 11 Bankruptcy When:

Multiple creditor classes with competing interests require comprehensive resolution. Bankruptcy provides a single forum to address secured debt, unsecured bondholders, trade creditors, and litigation claims under court-supervised priority rules.

Automatic stay is essential for businesses facing multiple foreclosures, lawsuits, or aggressive collection actions. The immediate, comprehensive creditor freeze provides critical breathing room.

Debt discharge represents the primary goal. When overwhelming unsecured liabilities require elimination rather than just asset preservation, bankruptcy's discharge power is indispensable.

Contract rejection capabilities are needed. Bankruptcy enables debtors to reject unfavorable leases or agreements with court approval, thereby shedding obligations that impair their viability.

Actual reorganization is the objective. If the goal is to restructure debt and continue the business in the long term under existing ownership, Chapter 11 provides the legal framework for plan confirmation and implementation.

Subchapter V eligibility exists (debt under $3,024,725). The 56% plan confirmation rate, compared to traditional Chapter 11's lower success rates, makes Subchapter V materially more attractive for eligible businesses.

Choose Receivership When:

Single or a few secured creditors dominate the situation. When one lender holds most of the leverage and other creditors are limited, receivership provides focused asset preservation without the complexity of comprehensive bankruptcy.

Speed is paramount. For rapidly deteriorating assets, fraud risk, or market timing considerations, receivership's ability to deploy within days and resolve within months proves decisive.

Cost preservation is critical. Mid-market companies, where Chapter 11's several-percent fee burden would consume disproportionate value, benefit from the receivership's lower cost structure.

Creditor control is preferred. Secured lenders wanting an industry-expert receiver to manage operations and prepare for sale can nominate receivers and steer the process more directly than in debtor-driven bankruptcy.

Federal bankruptcy is unavailable or inadvisable. Cannabis operators, certain regulated entities, or businesses where bankruptcy filing triggers contract terminations must pursue state remedies.

Asset sale is the primary goal rather than comprehensive debt restructuring. Receivership facilitates the efficient sale of going-concern businesses or orderly liquidations.

Industry-Specific Considerations

Cannabis operators face unique constraints. Federal bankruptcy remains unavailable due to marijuana's Schedule I status, with bankruptcy courts routinely dismissing cases involving plant-touching cannabis businesses. The multi-billion-dollar debt maturity wall approaching 2026 creates acute pressure for refinancing. Receivership represents the primary viable restructuring path, though state-specific licensing requirements for receivers add operational complexity. Only operators maintaining early creditor dialogue, strict cash discipline, and proven store-level EBITDA are expected to navigate the shakeout.

Secured lenders focus on maximizing collateral recovery. First-lien positions recovering 68-78% drive strategy, with intercreditor agreement terms proving critical. Receivership avoids bankruptcy administrative expense dilution that erodes secured creditor recovery. Following In re 530 Donelson, lenders should recognize that receivership orders, even with broad powers, do not automatically prevent the debtor from later filing bankruptcy.

Small businesses face stark choices. Those with debt under $3,024,725 should carefully evaluate the 56% plan confirmation rate of Subchapter V before opting for traditional Chapter 11. Businesses exceeding the Subchapter V limit often find receivership more cost-effective than conventional Chapter 11, which sees plan confirmation in only low-double-digit percentages of cases while consuming several percent of assets in fees.

Sources

Bankruptcy Filing Statistics:

S&P Global Market Intelligence, "US corporate bankruptcies soar to 14-year high in 2024"

Epiq Global, "Total Bankruptcy Filings Increased 10 Percent in the First Half of 2025"

Default Rates and Recovery Data:

S&P Global, "2024 Annual Global Corporate Default And Rating Transition Study"

S&P Global Ratings, "North American Debt Recoveries May Trend Down For Longer"

Legal Analysis:

Proskauer Rose, "The Evolving New Normal: 2024 Private Credit Restructuring Year in Review"

Florida Bar Journal, "Florida's New Commercial Real Estate Receivership Act"

DIP Financing:

Subchapter V Analysis:

University of Connecticut Finance Research, "Small Business Reorganization Act Analysis"

U.S. Department of Justice, U.S. Trustee Program, "Subchapter V Small Business Debtor Cases"

Cannabis Industry:

Cannabis Law Now, "Cannabis Receiverships Are and Will Be on the Rise"

Crain's Detroit Business, "Top cannabis companies lost $2B in 2024"

MJBizDaily, "Fed rate cut could be game changer as cannabis industry debt maturity looms"

Government and Court Sources:

Conclusion

Bankruptcy and receivership serve fundamentally different strategic purposes. Bankruptcy prioritizes debtor relief and provides comprehensive debt resolution, while receivership focuses on creditor protection and asset preservation. Neither is inherently superior; appropriateness depends on the creditor structure, debt type, timeline urgency, and desired outcomes. The 2025-2026 distressed environment underscores the importance of selecting a remedy. With default rates projected to remain near double historical averages through mid-2026 and over $2 trillion in debt maturities approaching, stakeholders face heightened restructuring decisions. Early action preserves value. In bankruptcy, administrative expenses erode secured creditor recovery, as professional fees, committee costs, and quarterly U.S. Trustee fees compound over timelines exceeding 17 months. In receivership, faster resolution and lower cost structure protect stakeholder interests. These choices carry permanent financial consequences. Professional counsel with expertise in both federal bankruptcy law and state receivership proceedings provides essential guidance for navigating the decision matrix effectively. If you need help evaluating restructuring options for your business or assessing creditor recovery strategies in a distressed situation, please contact Brightpoint to schedule a consultation.

Brightpoint Team

Blog

Stay Updated with Legal Trends

Stay informed with strategic insights from our team on the legal developments that matter to your business.

From regulatory shifts in specialized markets to emerging trends in corporate transactions, we deliver the analysis you need to make informed decisions and stay ahead of the curve.

How can we help?

Let's discuss how we can support your business with tailored legal counsel.

How can we help?

Let's discuss how we can support your business with tailored legal counsel.

How can we help?

Let's discuss how we can support your business with tailored legal counsel.